Top 5 Insurance Technology Trends Reshaping India's Distribution Landscape in 2026

I have a habit of asking people I meet at insurance conferences one question: “What keeps you up at night?” The answers have shifted dramatically over the last three years. Not long ago, the answers were mostly operational—delayed claim settlements, commission disputes, or policy renewal follow-ups slipping through the cracks.

In 2026, that answer is almost universally some version of: “Technology. I’m worried I won’t keep up.”

This anxiety is understandable. The pace of change in insurtech—particularly in India—has accelerated to a point where what felt cutting-edge eighteen months ago is now table stakes. Having spent the better part of two decades working in and around India’s insurance distribution ecosystem (including building the technology infrastructure for some of the country’s largest intermediaries), I’ve seen these shifts coming. Some are genuinely exciting. A few are disruptive in ways the industry isn’t quite prepared for.

Here are the five trends that, in my view, will most significantly reshape how insurance is distributed, sold, and serviced in India in 2026.

1. 🤖 AI Moves from “Assistant” to “Decision Maker” in Underwriting

For the past few years, AI in insurance has been largely confined to customer-facing chatbots and basic rule-based automation. That era is ending rapidly.

In 2026, we are seeing a meaningful shift where AI—specifically Large Language Models (LLMs) combined with traditional machine learning—is being embedded directly into the underwriting and risk assessment pipeline. Insurers in India are beginning to use AI to process unstructured data at scale: medical records, satellite imagery for property risk, social behaviour signals, and historical claims data, all synthesized in near real-time to produce more nuanced risk scores.

For the intermediary—the broker or the IMF—this has a profound implication: the “time to quote” for complex commercial lines or group health policies is collapsing. Insights from Swiss Re Institute’s sigma research on the economics of digitalisation indicate that digital transformation leads to significant efficiency gains, including up to 10–20% cost savings across the value chain. When the insurer quotes faster, the intermediary who has their client data structured and ready will close faster too.

What this means for you: If your client data is still locked in PDFs and spreadsheets, you’re going to struggle to participate in this new speed game. Agencies that have invested in systems that automatically parse, structure, and store policy and client data will have an enormous advantage. The broker who can pull up a client’s complete risk profile—across all their policies, past claims, and coverage gaps—in under 60 seconds, will win the relationship.

2. ⚙️ “Straight-Through Processing” Becomes the New Benchmark

Straight-Through Processing (STP)—the ability to issue, renew, or endorse a policy with zero human intervention in the data pipeline—is no longer a luxury for large broking houses. In 2026, it is becoming the expectation for even mid-tier intermediaries.

The driving force behind this is the expansion of insurer API ecosystems. Major Indian insurers have progressively opened up their systems to third-party integrations, allowing accredited intermediaries to connect their agency management systems directly to insurer platforms for real-time quotes, policy issuance, and data exchange.

The downstream effect is remarkable. An intermediary with STP capability can renew a motor policy for a client in under two minutes, from quote to policy document in the client’s inbox—without a single manual keystroke. For a broker managing 5,000 motor renewal accounts, this is the difference between a team of 20 and a team of 4.

McKinsey & Company’s Global Insurance Report highlights that P&C (Property & Casualty) insurers and intermediaries who embrace modern digital operating models, API-first architecture, and automation see substantial reductions in operational friction and a significant improvement in customer satisfaction.

The key bottleneck is no longer willingness; it’s data readiness. You can only achieve STP if your client and policy data is clean, structured, and in a format the insurer’s API can consume. This is precisely why the investment in robust policy inwarding and data hygiene pays dividends far beyond the initial time savings.

3. 📡 Telematics and Usage-Based Insurance Reaches the Mass Market

Telematics-based insurance—where premiums are calculated based on actual driving behaviour, distance, or lifestyle habits—has been a talking point in Indian insurance for nearly a decade. The promise has consistently outrun the adoption. In 2026, that is finally changing.

The convergence of three factors has created a genuine inflection point:

- Smartphone penetration in Tier-2 and Tier-3 India has made device-based telematics viable for a far larger population without requiring dedicated hardware.

- IRDAI’s regulatory sandbox has given insurers the formal pathway to pilot and then mainstream UBI (Usage-Based Insurance) products.

- The data literacy of younger vehicle owners has increased substantially. A 28-year-old who tracks every step with a fitness app is not philosophically opposed to sharing driving data for a cheaper premium.

For brokers and agents, this creates a fascinating new conversation with clients. UBI is a fundamentally different sales dialogue than traditional insurance. It shifts from “here’s what you pay” to “here’s how you can earn a better premium through your behaviour.” Agents who understand this product category—and can advise clients on what it means for their specific driving profile—will stand apart.

The deeper opportunity here is the renewal stickiness that telematics creates. A client whose premium is linked to their ongoing data relationship with the insurer does not casually switch to a competitor at renewal. This is the kind of long-term retention that every broker dreams of.

4. 🔗 Embedded Insurance Quietly Disrupts Traditional Distribution

If you haven’t been paying close attention to embedded insurance, now is the time to start—because it is the trend with the most disruptive potential for the traditional distribution model.

Embedded insurance means insurance that is invisibly woven into the purchase of another product or service. When you buy a flight ticket on MakeMyTrip, you get the option to add travel insurance. When you take a two-wheeler loan from a fintech NBFC, group health cover is bundled into the EMI. When a farmer registers on an agri-tech platform, crop insurance is embedded in the onboarding flow.

According to projections shared in Bain & Company’s financial services insights, embedded finance and insurance ecosystems are redefining traditional channels, with embedded transactions expected to multiply as businesses integrate protection directly into digital customer journeys.

Does this threaten the traditional broker? Not necessarily—but it does change the calculus. The intermediary who positions themselves as a specialist in comprehensive risk review and cross-sell (finding the gaps that embedded products don’t cover) will remain indispensable. The intermediary who was essentially a policy-issuance gateway—adding no advisory value—faces genuine pressure.

The advisors and IMFs who thrive in a world of embedded insurance will be those who can demonstrate that they understand a client’s total risk picture: what the embedded policy covers, where the sub-limits are, what the exclusions miss, and what additional cover is needed. That requires a sophisticated CRM and client management capability, not just a policy register.

5. 🔐 Cybersecurity and Data Privacy Go from “IT Problem” to “Board Agenda”

Here is a trend that doesn’t always make the “exciting insurtech” lists but is, in practice, one of the most consequential for any intermediary running a digital operation in 2026.

As agencies and brokers have digitized their client data, the attack surface for cyber threats has expanded dramatically. An insurance agency holds extraordinarily sensitive data—PAN cards, Aadhaar numbers, bank account details, health records, and asset information for potentially thousands of clients. This makes them an attractive target for cybercriminals, especially as most agencies are perceived as having weaker security postures than large financial institutions.

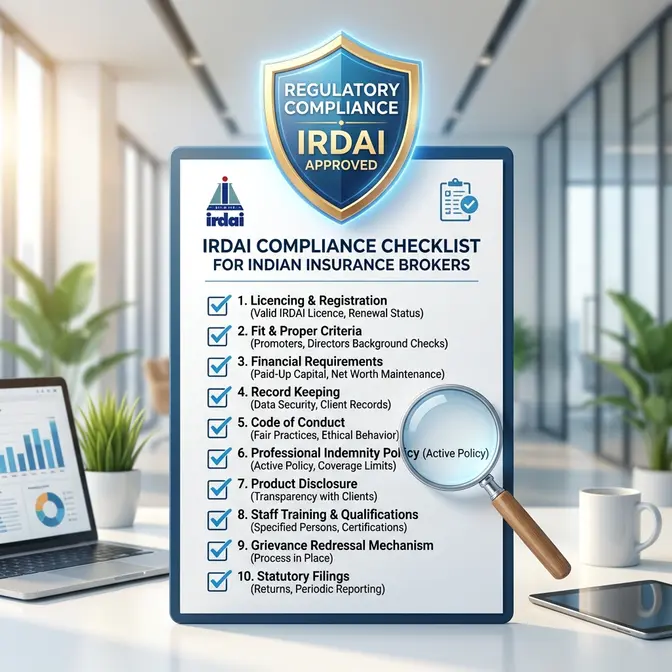

IRDAI has been progressively tightening the information security requirements for all regulated entities. The IRDAI (Protection of Policyholders’ Interests, Operations and Allied Matters of Insurers) Regulations, 2024 placed significantly greater obligations on data handling and breach disclosure. The ripple effect on intermediaries—who are custodians of much of this data—is only beginning to be felt.

Simultaneously, the business of cyber insurance itself is booming. India’s commercial lines cyber insurance market is growing at over 40% year-on-year as SMEs wake up to their digital risk exposure. For brokers, this represents an underserved product category with strong margins and very few genuinely informed advisors.

The agencies that will win in 2026 are those who practice good cybersecurity internally (demonstrating to clients that they are safe custodians of data) and become credible advisors on cyber risk to their commercial clients.

What Does This All Add Up To?

Reading these trends in isolation can feel overwhelming. But step back, and a single, cohesive picture emerges: the era of the generalist, paper-based, relationship-only insurance intermediary is definitively over. What’s replacing it is not a robot—it’s a technologically augmented expert.

The advisors, agencies, and brokers who will lead the market in 2026 and beyond share a common characteristic: they have invested in building a digital operational backbone—structured data, clean registers, insurer API connectivity, client CRM—that frees them to do what no algorithm can replicate: build trust, give nuanced advice, and be present at the moments that matter most.

One thing I’ve observed consistently across successful agencies—whether large broking houses or nimble two-person IMFs—is that the investment in the right technology platform pays back not just in efficiency, but in confidence. When your books are clean, your renewals are tracked, and your client data is structured and secure, you walk into any client meeting (or any IRDAI audit) with a fundamentally different posture. That confidence is, ultimately, a competitive advantage.

A Note on Staying Ahead

At IMD.Mitra, we built our platform specifically to help Indian intermediaries navigate exactly these transitions. Our AI-powered policy reader was designed because we knew that structured data was the foundation of every other trend on this list. Our insurer API integrations were built because STP is where the industry is heading. And our compliance-first architecture exists because we’ve seen what an IRDAI audit feels like when your records aren’t in order.

We’re not here to replace the advisor. We’re here to make sure that when these five trends accelerate—and they will—you’re already on the right side of them.

Want to see how IMD.Mitra is helping agencies prepare for the future of insurance distribution? Book a personalized demo and let’s talk about where your agency is today and where it needs to be.